Tim Hamilton, director of the Automotive United Trades Organization, the state’s service-station association.

OLYMPIA, July 19.—A modest little tax sold to voters with a noble purpose 24 years ago – sort of a state version of the federal Superfund cleanup program – has become one of the biggest cash cows in state government. It generates $300 million or so every budget cycle, sometimes more, and it pays for everything from local-government planning departments to the promotion of backyard compost pits. It has even bailed out the state itself when money is short. Now, after all these years, the Model Toxics Control Act is under attack in the state Supreme Court. A lawsuit would take most of that money and require that it be spent on highways.

It’s the kind of story that might make you think of golden geese. Tim Hamilton, director of the feisty service station association that brought the case, argues that the tax has always been unconstitutional. It’s a really a gas tax, he says, and the rule is clear — gas taxes are supposed to be spent on roads. But he says his group would never have sued if lawmakers had spent it the way voters intended.

“They went, oh jeez, look at this gold mine,” he says.

People just got too piggy.

The tax generates big money, somewhere between $150 million and $200 million a year at current gas prices. But a big chunk of the money doesn’t go where voters originally intended. Since 2005, some $290 million has been transferred or shifted from the hazardous waste cleanup fund. Lawmakers snatched most of that money, $233 million, to shore up the state budget in 2009-11. They diverted other money to unrelated Department of Ecology programs that faced big cuts. That essentially accomplished the same thing, but in a different way. And there’s more to the picture. You might say state officials have adopted a rather flexible attitude toward the use of the cleanup tax dollars — and clearly, it isn’t just about cleanup anymore.

Two years ago, after lawmakers drew the account down to zero in order to balance the budget, there was no protest from environmental groups. Instead they teamed with the governor to propose that the tax be tripled. Raise the tax and you might be able to clean up Puget Sound. Had the bill found one more sponsor in the Senate it might have passed. That’s when Hamilton’s group said enough. Now his lawsuit has finally reached the state’s highest court. It may soon decide whether a tax that sure looks like a gas tax really is one.

Two to Three Cents a Gallon

Tax receipts have skyrocketed with the price of gasoline.

The Supreme Court heard oral arguments June 14. Hamilton’s group, the Automotive United Trades Organization, contends that the bulk of the state’s hazardous substance tax really is indistinguishable from a gas tax. It is a levied as a percentage of the value of so-called hazardous substances – seven-tenths of a percent — on some 8,000 chemicals, pesticides, fertilizers, and oil products. But in a major sense it really is a fuel tax. Some 85 percent is paid by the oil refiners of Puget Sound, and of course, a big chunk of their production is sold in the state of Washington as motor fuel. Exactly how much money is at stake isn’t clear – apparently no one has done that calculation. But industry sources have done it the other way around. In recent years, the hazardous substance tax has added about two to three cents to the price of a gallon of gas, depending on how high the fuel price has gone.

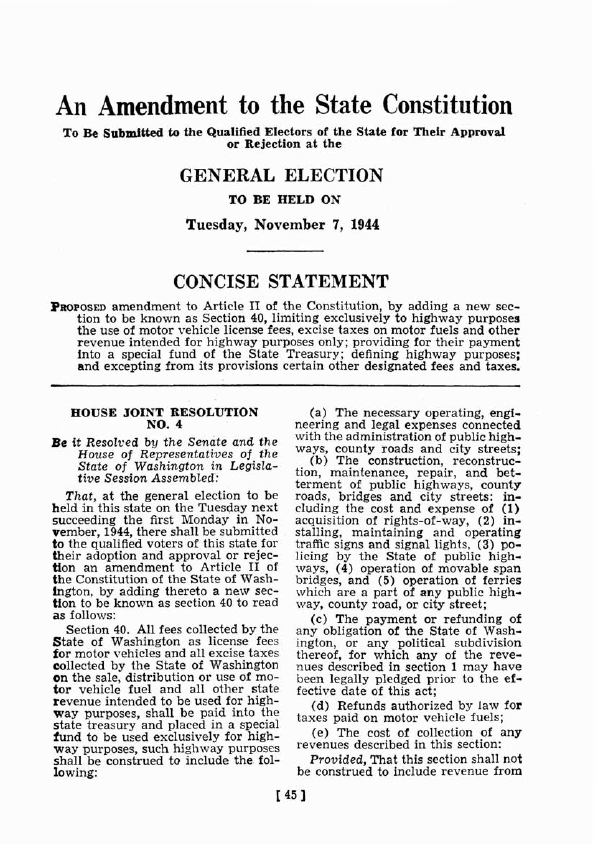

The voters did say yes to the tax in 1988 when they passed Initiative 97. But the state constitution takes priority over any initiative. And a 1944 amendment to the state constitution, the 18th, lays down a strict rule that transportation interests and courts have seen as sacrosanct. Gas-tax money has to be spent for roads, period. That hard-and-fast rule has been used over the years to defeat legislative moves to spend the money for other purposes, particularly transit. It comes down to the precise wording of the amendment, which bars the diversion of “all excise taxes collected by the state of Washington on the sale, distribution or use of of motor vehicle fuel.”

If it Looks Like a Duck

Phil Talmadge, the former state Supreme Court justice who is pressing the case for AUTO.

Hamilton’s group isn’t looking to toss out the tax after 24 years. What it’s saying is that the money derived from motor fuel needs to be deposited in the state motor vehicle fund. Phil Talmadge, the former Supreme Court justice who is pressing the case on AUTO’s behalf, is a former lawmaker himself, and he supported Initiative 97 when it came before the Legislature during the 1988 session. Today he argues that if it looks like a gas tax and it operates like a gas tax, then it’s a gas tax. Certainly it’s an excise tax. Certainly it’s a tax on motor fuel. Talmadge refers to the voters’ pamphlet of 1944 and the legislative debates on the issue. “I think it is safe to say that what we the people clearly indicated in the voters’ pamphlet was, keep your hands off anything that touches upon motor fuel,” he told the court last month. “Don’t touch this. It is a user fee. We want the revenue from that source to go into the motor vehicle fund, to be used for highway purposes.”

Taking the other side is the state attorney general’s office. It maintains that the hazardous substance tax is not a gas tax, because it affects products other than motor fuel. During the hearing, Laura Watson of the attorney general’s office noted that the 18th amendment exempts some taxes – “revenue from general or special taxes or excises not levied primarily for highway purposes.” Surely the hazardous substances tax meets that test, she argued.

“What is wrong with that [argument] is that it takes language in isolation out of the enacting clause and it starts with the assumption that any tax that even touches on gasoline must certainly be subject to the 18th Amendment,” Watson said. “What this [exemption] tells us that the voters also intended to preserve future taxing ability by the Legislature, or in this case, by the people, to enact taxes that might otherwise fall within the enacting clause.”

The 1944 voters’ pamphlet outlines what became known as the 18th Amendment.

Talmadge’s counter? He says the exemption was meant for the sorts of taxes that existed in 1944, like the business and occupations tax and the motor vehicle excise tax. Those taxes clearly covered different types of activities. The concern 68 years ago was that because they had something to do with motor fuel, at least in some cases, there needed to be some language to establish that they could remain in place. The statement from proponents that appears in the 1944 voters’ pamphlet appears to support the idea that the exemption was limited. It says simply, “This does not include the excise taxes levied for school purposes.”

Talmadge says the state is now trying to argue that the way the money is spent makes a difference, but what really counts is what is taxed and how the tax functions. He told the court, “The argument that the state advances is that basically the Legislature – and this is the core and substance of the state’s argument – the Legislature can say this is a gas tax in every way you can conceive of it, but if we say it is a gas tax for education, the 18th Amendment doesn’t apply. Well, so much for the anti-diversionary purpose of the 18th Amendment. That is precisely what the people who were the proponents of the 18th Amendment were trying to prevent.”

Why So Long?

An underground storage tank is removed during a cleanup project.

The surprising thing about the lawsuit may not be that it was filed, but rather that it took so long. Back in 1989, there was plenty of speculation that the oil and transportation interests might file a suit with precisely the same basis. But they struck a deal with the Legislature under which they thought tax revenue would never be allowed to rise, and so they never did. That thought went out the window, of course, when gas prices skyrocketed, from less than $1 a gallon in 1988 to as much as $4 today. The first full year, the tax generated a little over $40 million; this last fiscal year, thanks to the oil-price spike this spring, the state got $197 million.

Hamilton maintains the deal was between the Legislature and the big boys, but the service station operators weren’t part of it. The state argues he’s blocked from suing, too. Truth be told, Hamilton is one of the few left who actually remembers the dealmaking of more than 20 years ago. Perhaps a handful of veteran lobbyists and reporters might recall, however, that there is a big difference between what was said at the time and the way people perceive the tax today. Environmental groups wrote the initiative, and during a heated campaign that summer they toured the newspaper editorial boards of the state. Back then, I-97 was all about cleanup.

The 1988 voters’ pamphlet.

The initiative aimed to satisfy one of the big festering concerns of the day, the Love Canals of Washington — sites that had been polluted by companies that were no longer in business and for which no one could be held responsible. The measure established a process for assigning liability for cleanup, and it gave existing businesses an assurance that cases could not be reopened after plans were approved by the Department of Ecology and completed. The hazardous substances tax targeted the same types of chemicals that were responsible for the pollution, so at least there was some connection. About half the money went to the state; the other half to local-government cleanup programs.

The slogan that year, which appeared in the voters’ pamphlet, was “make the polluters pay,” and one can see that the description was all about the cleanup program – not a word about anything else. The initiative went on for page after page with rules for the cleanup process. Lawmakers put a business-backed alternative on the ballot, 97-B. All that summer you heard about “the dirty B,” and “B for business – B for bad.” The environmentalists won.

Not Many Restrictions

Over the years, the hundreds of millions of dollars generated by the tax paid for hundreds of costly cleanup projects – scooping out contaminated dirt, flushing out ground water. A report from the Department of Ecology in 2010 estimated that perhaps 400 known orphan sites remained at that point, and that they might be cleaned up over 10 years for just $50 million. New sites join the list every year, but the tax generates more than enough to cover the original purpose.

A Powerpoint slide from a Department of Ecology presentation shows how sweeping authority is derived from a broad statement in the intent section of Initiative 97.

A hearing before the House Environment Committee June 26 made it clear just how expansive the new vision for the tax money has become. “MTCA is actually a pretty broad statute,” said Ecology director Ted Sturdevant. “A lot of people think of it as a cleanup statute.”

So he pointed to a line from the law, reproduced on a Powerpoint slide: “Beneficial stewardship of the land, air and waters of the state is a solemn obligation of the present generation for future generations.”

From that intent clause, the state derives the idea that the tax can be used for other purposes – state and local solid waste planning, management, regulation, technical assistance, and public education. Reduction and recycling of hazardous wastes from households, small business and agriculture. Water programs. Air-pollution programs. Even hazardous waste cleanup.

Nothing says that can’t be done. Even if the initiative hadn’t made a sweeping statement in the first few paragraphs, the Legislature could always rewrite it. After two years, it takes only a simple majority vote to change an initiative. Lawmakers have done that on occasion, diverting MTCA money to things like shoreline planning, which might not be encompassed by the opening phrase. They also changed the law when they simply plucked money out of the account and put it in the general fund.

The money might help backstop the big cuts that have been necessary in time of recession, but critics say the purposes have become so diffuse that the hazardous substance tax is less a cleanup fund than it is a catch-all endowment for the Department of Ecology. It’s a worry for the petroleum industry. Every time there’s a diversion, there’s pressure to step up the tax. At the height of the debate in 2010, for instance, right after lawmakers snatched the money for the budget, Gregoire’s argument was that the tax rate ought to be tripled in part because the tax rate had never been increased. It just wasn’t keeping pace. That was despite the fact tax revenue already had gone through the roof because of the increase in oil prices.

“The tax has been generating more and more money over its history, basically driven by oil prices,” said Frank Holmes of the Western States Petroleum Association. “We still have a lot of cleanup sites around the state that could benefit from the MTCA fund if it is used for that purpose. But we don’t see that there’s any need to increase the tax rate or add more money to it. We need to focus the money on its intended use, which is cleaning up contaminated sites around the state.”

It’s one of the reasons the case before the Supreme Court is significant. If Hamilton’s group wins, the state may be hard pressed to maintain cleanup programs, much less all the other new purposes it has found for the money. But Hamilton says if the 18th Amendment, one of the clearest passages in the constitution, doesn’t provide a limit, nothing does. He says, “If the decision comes down against us, every motorist in the state had better get ready to take it right in the wallet.”

Your support matters.

Public service journalism is important today as ever. If you get something from our coverage, please consider making a donation to support our work. Thanks for reading our stuff.